Once an arcane corner of the capital markets, liability management exercises (LMEs) have become a mainstream restructuring tool. Of course, LMEs are not available to every borrower — the ability to execute one depends on loan documents that were deliberately drafted with this kind of flexibility. Facing debt maturities and/or tight liquidity, borrowers with the ability to do so are increasingly opting for these complex, out-of-court transactions in place of more traditional amend-and-extend deals or formal in-court restructurings. But do LMEs actually fix businesses?

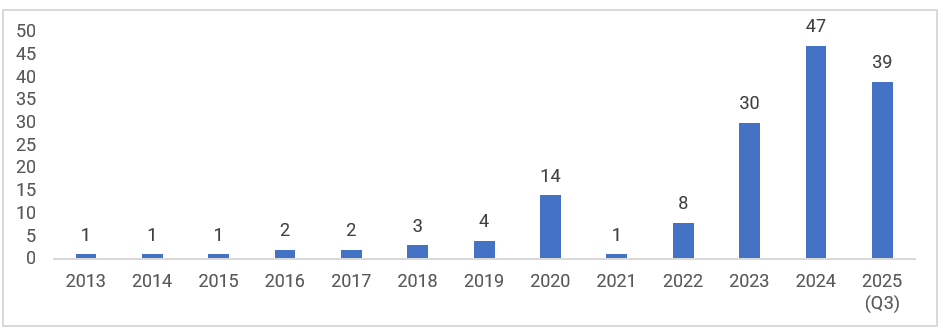

Based on data compiled by CreditSights (Figure 1), LMEs reached a record level in 2024 with that momentum continuing through Q3 2025. Pitchbook reported that LMEs now make up 65% of default activity by count. At the 2025 peak, LMEs comprised 73% of the default landscape whereas, in January 2020, the LME share was just 9%.

Figure 1: The Dramatic Rise of LMEs in the 2020s Source: CreditSights

This article examines whether LMEs simply delay an inevitable reckoning or can serve as a genuine bridge to recovery, buying time for a real operational turnaround. That question hinges on an often-under-emphasized distinction: the difference between balance-sheet restructuring and operational restructuring. For distressed companies and their stakeholders, the answer depends less on the elegance of the legal structuring and more on whether the underlying business can be fixed — and whether the extra time is actually used to do so.

Balance Sheet vs. Operational Restructuring

Restructuring work is often discussed as if it were monolithic. In practice, the exercise involves two distinct but interdependent efforts: restructuring the balance sheet and restructuring the operations.

Balance sheet restructuring is fundamentally about capital structure — reducing funded debt, extending maturities, changing priority and collateral, cutting cash interest, and reallocating value among creditors and shareholders. LMEs — as tools to reslice the liability stack without a formal insolvency process — belong squarely in this domain.

Operational restructuring is about the economics of the business itself. It addresses whether the company earns an adequate return on capital and generates sustainable cash flow. That involves rethinking pricing, product and customer mix, go-to-market strategy, cost structure, footprint, working capital discipline, and sometimes management.

Balance sheet and operational restructuring interact, but they are not interchangeable. A company in secular decline — such as a physical media retailer facing streaming or a legacy print directory business in the age of search — cannot deleverage its way back to relevance without a strategic pivot. Conversely, many operationally sound borrowers with temporary setbacks or self-inflicted wounds (such as poor capital allocation, undisciplined expansion, neglected working capital management) can be rehabilitated through balance sheet relief, provided they are given time and liquidity and management is willing to act.

An LME can affect only one of these dimensions directly. It can ease the financial pressure. It cannot, by itself, improve customer retention, develop a better product, or cure a structurally uncompetitive cost position. That distinction is often lost in the rush to “solve the debt problem” before the next maturity wall.

The Rise and Evolution of LMEs

In the early phase (from the 1980s through the 2010s), transactions were relatively simple: exchange offers, consent solicitations, and amend-andextend deals that pushed out maturities in exchange for higher pricing and modest covenant changes. The foundational case, Katz v. Oak Industries in 1986, established the legality of exit consents.

As documents loosened and sponsors became more aggressive, a second phase (2016-2019) emerged, marked by “layer cake” capital structures and creative use of baskets, investment capacity, and unrestricted subsidiaries to establish priming or structurally senior debt. This era, exemplified by the J. Crew drop-down, popularized two general transaction types — drop-downs and uptiers.

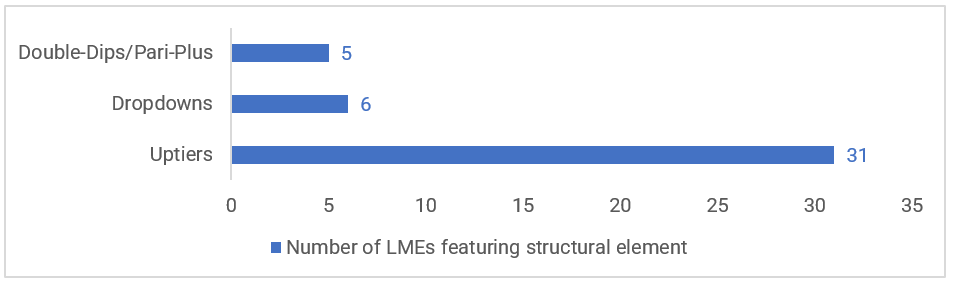

The recent wave (2020-present) introduced new structural innovations, including double-dips/pari-plus and hybrid LMEs (Figure 2). This period has also witnessed intense lender litigation. High-profile fights over uptier exchanges — such as Boardriders and TriMark — and drop-downs transactions have demonstrated both the power of documentation and the willingness of disadvantaged creditors to litigate, creating an increasingly litigation-aware environment. The response has been two-fold:

- More cautious structuring approach in some quarters — using exchange-and-extend mechanics or other routes to achieve non-pro rata outcomes with a better litigation posture.

- An arms race in new documentation, with “blocker” provisions and anti-“trapdoor” protections designed to prevent the most aggressive forms of creditor-oncreditor maneuvering.

The rise of private credit has become an increasingly important part of the story.

Figure 2: LMEs From Q12025 Through Q32025 Source: CreditSights

These funds now participate in, or even drive, LMEs that historically would have been the preserve of broadly syndicated loan (BSL) and bond markets. The shift to smaller, more concentrated lender groups can speed up decision-making, but frequently results in more tailored documentation and a wider variance of outcomes across transactions.

In this environment, LMEs are not an exotic anomaly but a routine feature of the restructuring landscape. The question is not whether they will continue, but whether they are being used responsibly and to what end.

When an LME Is Just a Bandage

The Band-Aid critique starts with the obvious: LMEs are primarily financial engineering. They rearrange claims on cash flows without necessarily changing the cash flows themselves. When deployed without a credible operational plan, they tend to extend the life of a struggling business without improving its prospects.

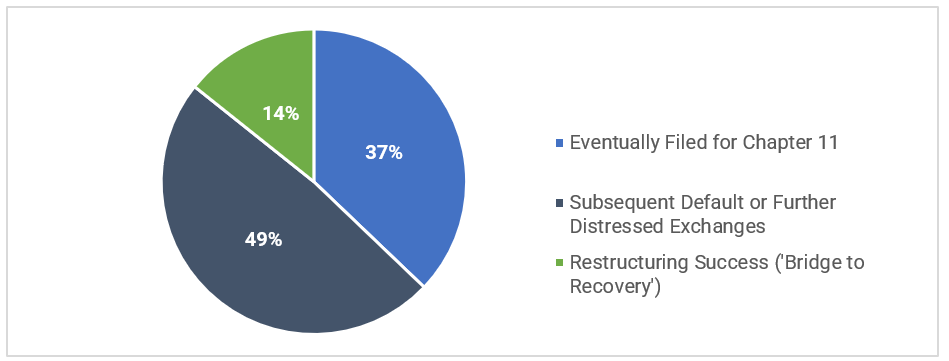

S&P Global Ratings tracked 35 companies executing 38 LMEs from mid-2017 through August 2024 — only five (14%) staved off subsequent bankruptcy or default (Figure 3).

Figure 3: LMEs Alone Cannot Address Drivers of Distress

Several Recurring Features Characterize Bandage LMEs

- Failure to address business fundamentals: If the core issue is eroding market relevance or structurally high costs, a modest reduction in cash interest or maturity push does little more than slow the pace of deterioration. The company may avoid near-term default, but it emerges with the same strategic problems and fewer options, because the easiest levers — cheap refinancing and covenant flexibility — have been spent.

- Incremental leverage and cost: Many LMEs require “consent fees,” new-money tranches at premium pricing, or sweeteners to incentivize participation by key creditor groups. Ironically, this can increase the total debt burden, at least initially, and raise the blended cost of capital. If the transaction is executed under duress, with weak negotiating leverage, the company may be exchanging one unsustainable profile for another. S&P noted that the post-LME total first-lien debt generally increased for most because these transactions were more focused on improving liquidity than bringing distress drivers to more sustainable levels.

- Fragmented capital structures and litigation risk: Aggressive LMEs, particularly those creating priming debt for a creditor subset, can generate what is known as creditor-on-creditor violence. Disadvantaged creditors respond with litigation, injunction requests, and parallel negotiations. Management time and cash intended to support operational initiatives are instead consumed by legal disputes and investor relations.

- Minimal quantum of relief: An LME that reduces annual cash interest by a few percentage points or extends maturities by a year, without addressing excessive leverage, may simply act like a bandage, cosmetically covering the wound (by delaying an imminent default or bankruptcy filing) while the underlying condition worsens.

In short, when an LME is undertaken without a contemporaneous operational turnaround plan, it reliably increases capital structure complexity without improving underlying business viability.

When an LME Can Be a Bridge to Recovery

The case for LMEs as a bridge to recovery rests on their ability to create time and flexibility — scarce resources in a distressed situation — and to do so out-of-court, potentially preserving more value for the overall estate.

Several conditions support this constructive role:

- Extending the runway meaningfully: An LME that pushes out maturities by several years can give management room to execute substantial operational programs, such as closing underperforming locations, renegotiating major contracts, investing in research and development (R&D), or rationalizing overhead. This time extension is particularly valuable for businesses whose problems are remediable — those reacting to cyclical downturns, transient cost shocks, or fixable strategic missteps rather than terminal disruption.

- Genuine deleveraging: Exchange offers that capture market discounts — swapping debt trading below par into new instruments at or closer to par — can reduce funded debt without cash outlay. When executed at sufficient scale, this improves leverage and coverage metrics, immediately and visibly.

- Enhanced financial flexibility: A well-structured LME can rationalize covenants and baskets in a way that supports the turnaround plan. Resetting terms in legacy documents — often reflecting an earlier phase of the company’s life cycle — can block opportunistic value transfers while preserving carefully tailored capacity for acquisitions or investments genuinely tied to the recovery strategy.

- Avoiding the costs of formal insolvency: Out-of-court solutions prevent the direct costs of Chapter 11 — such as professional fees, Debtor-In-Possession (DIP) financing costs, and court oversight — and the indirect costs of customer and supplier anxiety while preserving intangible value associated with brands and contractual relationships that would otherwise be impaired.

In these cases, an LME does more than shift debt — it underwrites a broader restructuring plan by transforming the capital structure from a constraint into a catalyst for operational change.

Carvana’s 2023 debt exchange, for example, served as a textbook “bridge.” Facing a cyclical downturn in the used car market, the company executed an offensive exchange, trading unsecured notes for new secured debt at a discount. This reduced total debt by over $1.2 billion, extended maturities through 2028-2031, and significantly cut near-term cash interest. Crucially, this bought management the runway needed to improve unit economics and wait out the market dip. The company turned profitable in 2023, from a loss of $216 million a year earlier, demonstrating genuine operational improvement versus just financial engineering and avoiding the value destruction of a bankruptcy filing.

The Core Filter — Is the Business Viable?

The most important question in assessing any LME is deceptively simple: Is the business fundamentally viable once restructured?

That assessment is not about heroic projections. It requires a candid view of industry structure, competitive dynamics, and secular trends, plus an evaluation of whether, under realistic operating assumptions, the business can generate free cash flow and earn a reasonable return on capital after the transaction.

When the answer is “yes, with changes,” an LME can be a rational tool. In such cases, capital structure relief provides breathing room to execute clearly defined operational initiatives: pruning unprofitable lines, consolidating facilities, improving pricing discipline, or reorienting the sales force.

Where the answer is “no,” the LME becomes a way to postpone a necessary reallocation of assets. In that context, the more aggressive the LME, the more it resembles a value transfer among creditors rather than a genuine rehabilitation.

Turnaround professionals, therefore, view LMEs not as a standalone product but as one instrument in a broader toolkit. The quality of the LME is inseparable from the quality of the underlying turnaround plan.

Timing, Tactics, and Creditor Dynamics

Timing is the second critical variable. The same structure can function as a bridge or a bandage depending on when it is executed.

An offensive LME is undertaken while the company still has liquidity and negotiating leverage. Management can approach creditors proactively, seek broad participation, and design a transaction that balances stakeholder interests. Such deals are more likely to achieve meaningful maturity extensions or deleveraging at a manageable cost.

A defensive LME, by contrast, is typically executed against the clock — a looming maturity, covenant breach, or liquidity shortfall. Creditors demand steeper economic terms and are motivated to engage in complex priming/dropdown structures that favor select groups, deepening intercreditor conflict.

Creditor composition also matters. A concentrated group of sophisticated lenders can facilitate swift decision-making and support holistic solutions. A fragmented investor base, including funds with divergent mandates/time horizons, is more likely to produce holdout problems and tactical litigation. Creditors are forming “coops” to present a united front, with some agreements covering just 51% of a loan to maintain optionality.

Sponsor-backed deals can cut both ways: Sponsors may have the incentive and capital to support new-money transactions but may also pursue aggressive structures to preserve equity value.

The best bridge LMEs tend to share certain traits, such as high participation rates, relatively simple mechanics, and an explicit link to a turnaround plan that is communicated to creditors. Market participants note that LMEs have evolved since 2020’s non-pro rata transactions, moving toward tiered structures where everyone participates at some level. The weakest Band-Aid deals are often opaque, heavily engineered, and accompanied by only vague references to operational change.

The Documentary Arms Race

Finally, the feasibility and character of future LMEs are increasingly shaped by the documentation environment. The last cycle of aggressive LMEs prompted a buy-side counter-reaction: tighter transfer restrictions, limits on unrestricted subsidiary designations and investment/asset transfer baskets, and explicit “anti-drop-down” language. While some blockers (e.g., J. Crew) have become de rigueur buy-side asks, others tend to appear only in post-LME financings or in more bespoke/challenging financing arrangements.

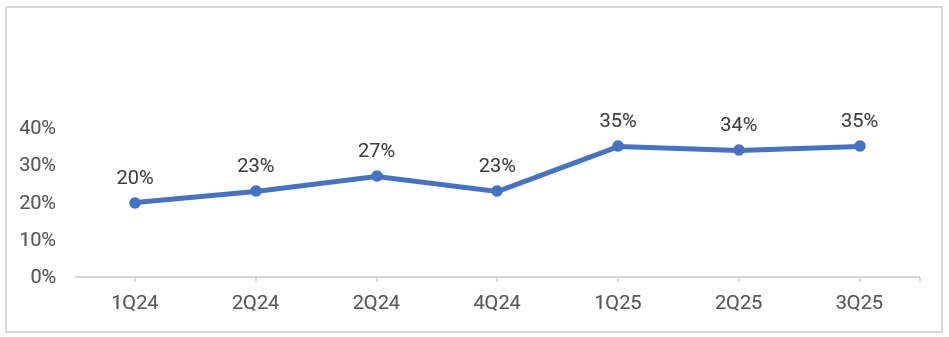

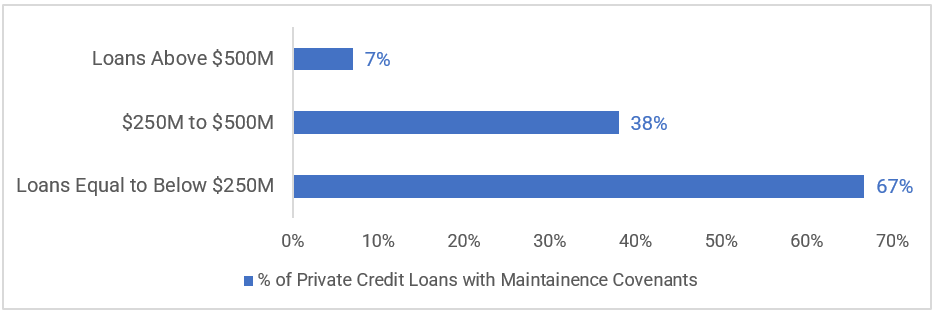

Yet the market’s response remains inconsistent. Despite high-profile litigations, many new deals continue to preserve flexibility for aggressive LMEs (See Figure 4). More noteworthy, many outstanding loans still contain the loopholes exploited in previous LMEs while private credit documentation has shown signs of loosening (See Figure 5).

This scenario has two implications:

- It increases the importance of careful documentary review when assessing options. How a blocker or basket clause is worded can determine whether a creative LME is even possible.

- It may help shift behavior over time from the most aggressive forms of creditor-on-creditor conflict toward more consensual transactions. For practitioners focused on operational recovery, this may be a welcome development. Complexity for its own sake rarely improves the odds of a successful turnaround.

Figure 4: New BSL Deals Allowing Privately Negotiated Buybacks/Omitting “Open Market Purchase” Language

Figure 5: Maintenance Covenants Across Deal Sizes

LMEs as a Tool, Not a Cure

LMEs were the natural next step in the leveraged-loan documentation arms race, with covenant-lite structures and elevated interest rates throwing fuel on the fire. One thing is certain — LMEs will remain a recurrent fixture in corporate restructuring, notwithstanding growing scrutiny of their risks.

But an LME is not a cure-all. It is a tool for reallocating risk among stakeholders and buying time. Used early, alongside a realistic operational plan, it can be a bridge to recovery, extending runway and aligning the capital structure with the company’s potential. Used late, without a credible turnaround agenda, or primarily as an intra-creditor value-transfer mechanism, it becomes a bandage, at best postponing the inevitable and at worst adding litigation costs and further value destruction.

For restructuring professionals, the practical question is therefore not whether to favor or oppose LMEs in the abstract, but how to evaluate their purpose in any given situation. That evaluation should start with three simple questions:

- Is the underlying business model viable?

- Does the transaction deliver meaningful and sustainable relief?

- Is the time bought by the LME clearly earmarked for specific operational changes?

When the answer is yes, LMEs can play a constructive role in saving businesses. Otherwise, they merely defer the inevitable reckoning, often at a higher ultimate cost.

This article was first published with the Journal of Corporate Renewal.

© Copyright 2026. The views expressed herein are those of the author(s) and not necessarily the views of Ankura Consulting Group, LLC, its management, its subsidiaries, its affiliates, or its other professionals. Ankura is not a law firm and cannot provide legal advice.