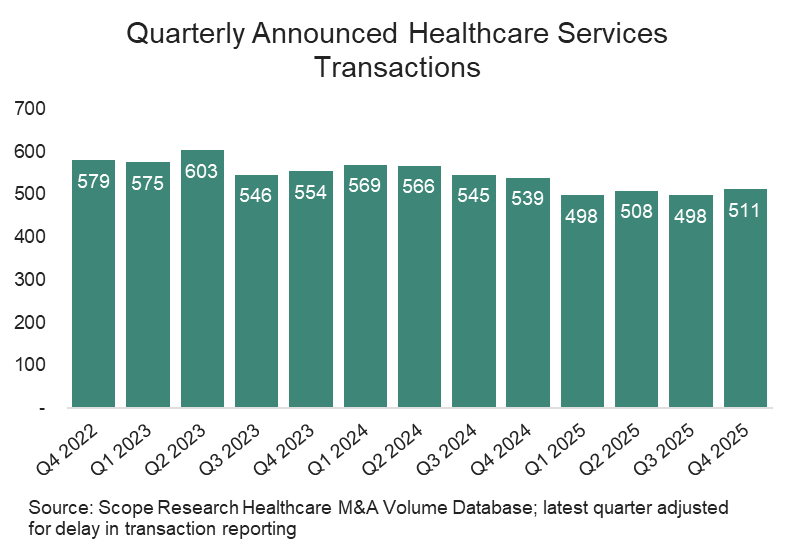

Ankura is pleased to present an overview of healthcare services transactions announced or closed during Q4 2025 in the United States. Total transactions increased by 2.6% in the fourth quarter of 2025 after decreasing by 2.0% in the third quarter. However, compared to Q4 2024, transaction volumes for Q4 2025 were down by 5.2%.

Notable Transactions Announced or Closed in Q4[1]

- Thermo Fisher Scientific Inc. entered into a definitive agreement on Oct. 29, 2025, to acquire Clario Holdings, Inc. for approximately $8.9 billion, implying a 7.1x price to revenue multiple and a 19.0x price to Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) multiple. Clario is a clinical trial technology company providing data management and endpoint technology to pharmaceutical and biotechnology companies developing new drugs. The company’s platform has supported approximately 70% of Food and Drug Administration (FDA) drug approvals over the past decade.

- Vanderbilt University Medical Center entered into a definitive agreement to acquire the remaining 80.0 percent interest in Tennova Healthcare – Clarksville from Community Health Systems (NYSE:CYH) on Nov. 4, 2025. The purchase price equates to an enterprise value of $750 million, implying a 3.3x price to revenue multiple and a 19.0x price to EBITDA multiple. Vanderbilt has held a 20.0% minority interest since 2021. The acquisition included the 270-bed main hospital campus, a freestanding emergency room, and related physician clinics and outpatient services.

- GE Healthcare entered into a definitive agreement on Nov. 20, 2025, to acquire Intelerad for $2.3 billion, implying an 8.5x price to revenue multiple. Intelerad is a medical imaging software company based in Canada, which provides radiology workflow and imaging solutions to healthcare providers worldwide. According to reports, the company’s products are relied upon by over 1,500 healthcare organizations.

- Abbott entered into a definitive agreement to acquire Exact Sciences (NASDAQ: EXAS) on Nov. 20, 2025, for $105 per share, or $21 billion. The proposed terms indicate a 6.4x price to revenue multiple. Exact Sciences develops and distributes screening and diagnostic test products both in the U.S. and internationally, specializing in non-invasive cancer screenings.

- Cencora entered into a definitive agreement to acquire the remaining 65.0% interest in OneOncology on Dec. 15, 2025, for approximately $4.8 billion, implying a 19.0x price to EBITDA multiple. Cencora had previously acquired a 35.0% interest with the option to purchase the remainder. OneOncology operates as a network of 29 independent community oncology practices with approximately 1,800 providers throughout the U.S.

Key Observations

The fourth quarter of 2025 saw a slight increase in transaction activity for the healthcare services industry. However, the number of transactions remained below activity for the fourth quarter of last year. The Federal Reserve continued to reduce rates, announcing 25 basis point cuts at meetings in October and December. Additionally, inflation continued to decline during the fourth quarter.

Federal oversight of healthcare acquisitions remained heightened, with a continued focus on private equity investment in healthcare and provider roll-up strategies. While some actions taken by the Trump administration signal a more business-friendly approach, such as long-awaited approval for UnitedHealth’s acquisition of Amedisys, the Federal Trade Commission’s (FTC’s) decision in February 2025 affirming retention of the prior administration’s stricter merger-guidelines framework continues to shape the regulatory environment.

Regulatory scrutiny at the state level continued to expand, particularly focused on healthcare transactions involving private equity. By the end of 2025, at least 15 states had enacted or expanded healthcare transaction review laws, with new proposals extending mandatory notification, pre‑closing review periods, and broader definitions of “material change” to include arrangements including management services organizations. Some states, such as Massachusetts and New Mexico, advanced legislation increasing review requirements, while others focused on increased transparency, cost‑impact reviews, and limits on corporate influence over clinical decision-making.

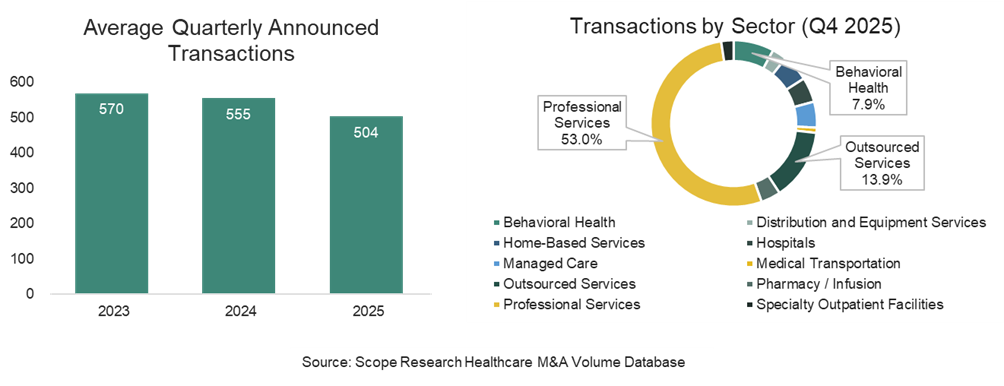

As shown in the figures below, recent healthcare acquisitions continue to be dominated by three sectors making up 74.8% of transactions in Q4: Professional Services,[2] Outsourced Services,[2] and Behavioral Health. The Professional Services sector remained the most active sector in terms of total transactions due to continued interest from health systems and private equity buyers alike, accounting for 53.0% of total deal volume.

In the Professional Services sector, most of the transaction activity was in Dentistry, with 108 announced transactions, and Physician Practices, with 105 transactions. Much of the activity in Dentistry is being driven by Dental Service Organizations (DSOs) acquiring and/or partnering with dental practices, including MB2 Dental, Heartland Dental, Smile Partners USA, Imagen Dental Partners, and Apex Dental Partners. While acquisitions in the Physician Practices sector included activity across several specialties, there was a notable concentration in Dermatology, Primary Care, and Orthopedics.

Activity in the Behavioral Health sector declined substantially in Q4, with total transaction declining 29.1%. This decline occurred across the addiction, IDD, and mental health sub-verticals, and is likely driven at least in part by the uncertainty of Medicaid coverage following the passage of the One Big Beautiful Bill Act (OBBBA). For more insights on the OBBBA, explore Ankura’s article diving into the implications of the OBBBA for the healthcare industry.

The Hospital sector was active in the fourth quarter with 24 announced transactions, remaining relatively consistent with Q3. Acquisitions were primarily driven by regional health systems looking to expand their market share through strategic acquisitions.

During the quarter, Ankura’s Transaction Advisory practice provided guidance on a diverse range of deals across the sector, including transactions in acute care hospitals, dentistry, behavioral health — spanning autism services, addiction treatment, and psychiatry — physician practices, and long-term care services.

2025 Healthcare Services M&A Review

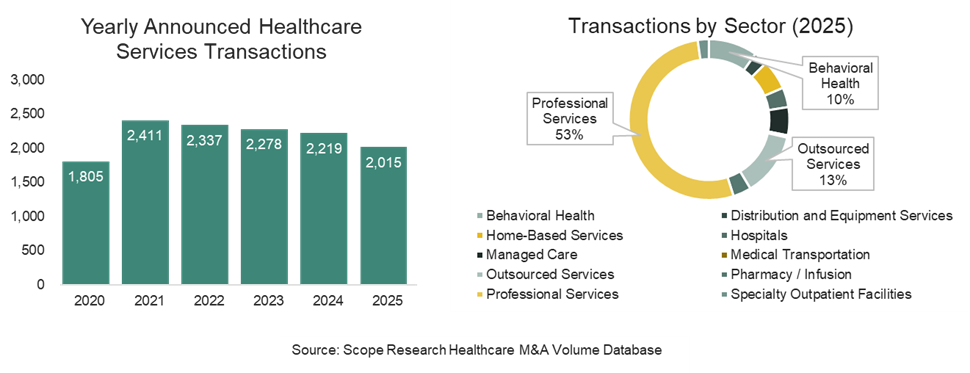

Deal activity over the past year has been influenced by a combination of pressures, including heightened regulatory uncertainty, shifting policy priorities under the Trump administration, and ongoing financial challenges stemming from declining reimbursement rates, tariffs, and persistent labor constraints. As such, the healthcare mergers and acquisitions (M&A) landscape saw another year of decline throughout 2025, pointing to a trend that has continued since the high levels experienced in 2021.

Overall deal volume dropped 9.2% across all healthcare services sectors relative to 2024, underscoring the challenges and shifts experienced within the industry. Particularly noteworthy was the Distribution and Equipment Services sector, which, despite a recovery in deal volumes in the fourth quarter, still saw a 36.0% decline relative to the prior year. Likewise, the Specialty Outpatient Facilities sector declined 31.8% relative to the prior year despite a 9.1% recovery in fourth quarter deal volumes. Professional Services, while remaining the most active sector, declined 13.2%, respectively, relative to 2024 levels.

Despite broader declines, certain healthcare sectors saw some growth in M&A activity. Although still below the levels seen immediately following the pandemic, Behavioral Health transactions increased 10.1% over 2024 and remained an active space for investors. The Medical Transport and Pharmacy / Infusion sectors also increased 12.5% and 12.3%, respectively, in 2025 relative to 2024.

Future Outlook

Looking toward 2026, healthcare investors will be closely monitoring the cost of capital, economic conditions, the regulatory landscape at both the federal and state level, and the impact of the Trump administration’s policy decisions. The Federal Reserve started 2026 by pausing rate cuts in January, and most economists are expecting rates to remain steady for at least the first half of the year. Inflation also declined relative to 2024, and investors will look for this trend to continue going forward.

At the federal level, The Trump administration has generally been viewed to be more business friendly and expected to have looser restrictions on M&A activity. However, the FTC’s decision to retain the merger-guideline framework previously held by the Biden administration in 2025 may signal that investors should expect heightened levels of scrutiny to remain.

Outside the federal regulatory process, various states have continued to introduce or enact legislation to increase regulatory scrutiny. This expansion of regulatory requirements at the state level could result in delays due to mandatory reviews, as well as investors focusing on certain markets with less stringent requirements.

Transaction activity going forward will also be shaped by the OBBBA’s impact on the healthcare industry. While the OBBBA includes several business-friendly tax provisions, the OBBBA’s sweeping changes to Medicaid enrollment and Affordable Care Act (ACA) marketplace coverage could have a significant impact on certain healthcare verticals.

Additionally, the Centers for Medicare and Medicaid Services (CMS) is increasing reimbursement for physician services for the first time since 2020. This 3.8% increase will slightly relieve margin pressures most operators are experiencing. For more insights, explore Ankura’s recent article discussing the key changes to physician reimbursement introduced by CMS.

Going forward, we anticipate an increase in transaction activity, with a more focused approach on specific geographic regions and healthcare sectors due to anticipated impacts from the OBBBA and regulatory scrutiny.

About Ankura Healthcare Transaction Advisory Services

Healthcare transactions are inherently complex. With deep industry experience, Ankura delivers insights to make informed investment decisions in mergers, acquisitions, and partnerships.

Ankura’s Healthcare Transaction Advisory team is deeply rooted in the healthcare sector, leveraging extensive industry knowledge and expertise to anticipate critical financial accounting aspects of transactions while also understanding the operational drivers. This enables us to proactively address critical financial accounting aspects and operational drivers of transactions.

What sets us apart is the collaboration between our financial accounting due diligence experts and Ankura’s specialized teams in healthcare valuation, healthcare operations, tax, information technology, commercial strategies, and human capital. This collaboration ensures a seamless, integrated reporting process to you, combining diverse expertise to provide a holistic view of every transaction. Our approach guarantees that you receive nuanced, actionable insights in a unified and strategic manner.

With senior deal professionals engaged in every transaction phase, we provide immediate updates on significant deal factors and a dedicated analysis of any critical issues, ensuring a thorough understanding and resolution of underlying concerns.

Learn more: Healthcare & Life Sciences Transaction and Valuation Advisory – Ankura.com

Sources

[1] Scope Research Healthcare M&A Volume Database, published by Scope Research; Capital IQ

[2] The Professional Services sector includes dentistry, physical therapy, physician practices, urgent care, veterinary, and other clinics. The Outsourced Services sector includes billing, revenue cycle, management services organizations, marketing, staffing, and other services commonly outsourced by medical practices.

© Copyright 2026. The views expressed herein are those of the author(s) and not necessarily the views of Ankura Consulting Group, LLC., its management, its subsidiaries, its affiliates, or its other professionals. Ankura is not a law firm and cannot provide legal advice.