Healthcare Services Transactions Update – Q1 2026

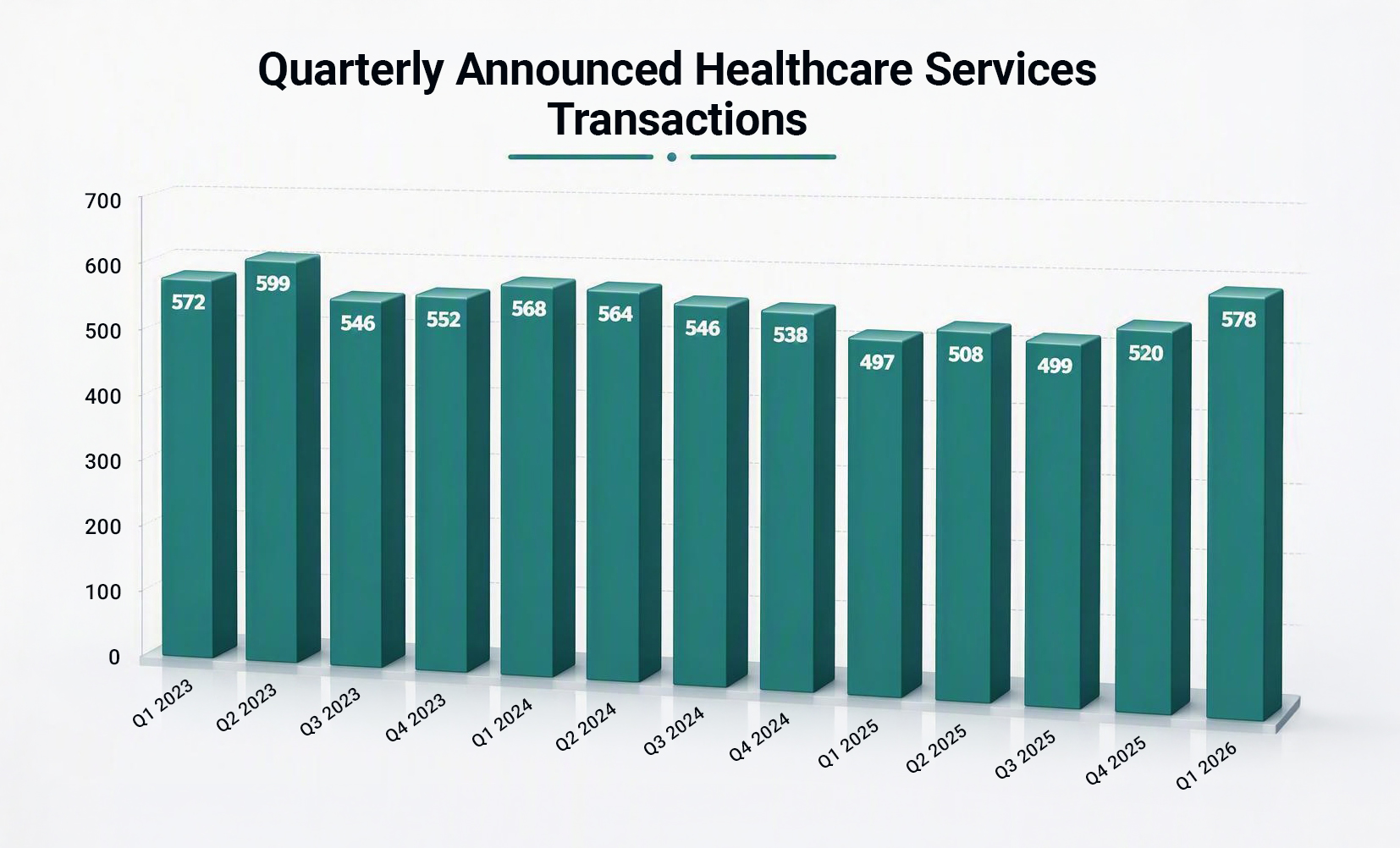

Ankura is pleased to present an overview of healthcare services transactions announced or closed during Q1 2026 in the United States. Total transactions increased by 11.2% in the first quarter of 2026 after increasing by 4.2% in the fourth quarter. Compared to Q1 2025, transaction volumes for Q1 2026 increased by 16.3%.

Notable Transactions Announced or Closed in Q1[1]

- Cencora, Inc. entered into a definitive agreement on March 23, 2026, to acquire EyeSouth Partners’ Retina Business for approximately $1.1 billion, implying a 1.47x price to revenue multiple and a 10.0x price to earnings before interest, taxes, depreciation, and amortization (EBITDA) multiple. The retina business will join Retina Consultants of America, expanding Cencora’s specialty physician platform in ophthalmology. EyeSouth’s retina network is part of a broader physician-led eye care organization supporting affiliated ophthalmologists and retina specialists.

- A consortium led by Welsh, Carson, Anderson & Stowe entered into a definitive agreement on March 2, 2026, to acquire Select Medical Holdings Corporation for $16.50 per share, representing an enterprise value of approximately $3.85 billion and implying a 0.67x price to revenue multiple and a 7.91x price to EBITDA multiple. Select Medical is one of the largest operators of critical illness recovery hospitals, rehabilitation hospitals, and outpatient rehabilitation clinics in the U.S., with a broad national footprint across post-acute care settings.

- Kinderhook Industries entered into a definitive agreement on Feb. 23, 2026, to acquire Enhabit, Inc. for $13.80 per share, valuing the company at approximately $1.11 billion and implying a 1.02x price to revenue multiple and a 10.09x price to EBITDA multiple. Enhabit is a national home health and hospice provider with a multi-state footprint, delivering in-home clinical care and end-of-life services through a large network of home health and hospice locations.

- Tenet Healthcare Corporation announced a transaction acquiring the remaining 23.8% stake in Conifer Health Solutions from CommonSpirit Health on Feb. 2, 2026, with total enterprise value of approximately $2.65 billion, implying a 13.95x price to EBITDA multiple based on 2025 adjusted EBITDA less noncontrolling interest. Conifer is a revenue cycle management and value-based care services platform serving hospitals, health systems, and physician groups through front-end patient access, mid-cycle clinical revenue integrity, and back-end accounts receivable management solutions.

- General Atlantic acquired TEAM Services Holding, Inc. in January 2026 for approximately $3.0 billion, implying a 1.25x price to revenue multiple and an 11.49x price to EBITDA multiple. TEAM is one of the largest providers of Medicaid-funded personal care and consumer-directed home care services in the U.S., offering agency-based home care, caregiver employment administration, and related support services across a broad national footprint.

- The University of Nebraska agreed on Jan. 2, 2026, to acquire Clarkson Regional Health Services’ remaining 50% interest in Nebraska Medicine for approximately $800 million, with total implied enterprise value of approximately $1.92 billion and implied multiples of 0.63x revenue and 5.7x EBITDA. Nebraska Medicine is the largest academic health system in Nebraska, anchored by Nebraska Medical Center and Bellevue Medical Center, with more than 800 licensed beds, an extensive specialty and primary care network, and a longstanding affiliation with the University of Nebraska Medical Center.

Key Observations

The first quarter of 2026 saw a significant increase in transaction activity for the healthcare services industry. This jump in total transactions — both over the previous quarter and year-over-year — occurred despite the Federal Reserve holding rates steady, slightly higher inflation during the quarter, and geopolitical conflict in the Middle East creating additional pressure through higher oil prices, broader market volatility, and renewed financing uncertainty.

Regulatory scrutiny of healthcare transactions also remained elevated during Q1 2026, particularly in deals involving provider consolidation, physician practice roll-ups, and private equity sponsorship. Federal oversight intensified during the quarter when the Federal Trade Commission (FTC) launched a dedicated Healthcare Task Force in March, reinforcing a more coordinated review of consolidation, serial acquisitions, and private equity-backed platform strategies.

State-level oversight also remained active in Q1, with regulators focused on private equity-backed deals and management services organization (MSO) structures. California’s expanded transaction notice requirements took effect on Jan. 1, 2026, increasing reporting obligations for certain transactions involving private equity groups, hedge funds, and MSOs. During the quarter, several states also considered or advanced legislation aimed at expanding disclosures, lengthening notice periods, and broadening review of roll-up strategies and other non-reportable affiliations.

As shown in the figures below, recent healthcare acquisitions continue to be dominated by three sectors making up 72.3% of transactions in Q1: Professional Services,[2] Outsourced Services,[2] and Behavioral Health. The Professional Services sector remained the most active sector in terms of total transactions due to continued interest from health systems and private equity buyers alike, accounting for 50.3% of total deal volume.

In the Professional Services sector, most of the transaction activity occurred in Physician Practices with 145 announced transactions and Dentistry with 88 transactions. While acquisitions in the Physician Practices sector included activity across several specialties, there was a notable concentration in Dermatology, Primary Care, and Ophthalmology. Much of the activity in Dentistry is being driven by Dental Service Organizations (DSOs) acquiring and/or partnering with dental practices, including MB2 Dental, SALT Dental Partners, Smile Partners USA, Imagen Dental Partners, and Heartland Dental.

Activity in the Behavioral Health sector increased substantially in Q1, with total transactions increasing 33.3%. This growth was driven particularly by heightened activity in the Intellectual and Developmental Disability (IDD) space, reflecting continued interest from strategic and private-equity backed buyers.

The Hospital sector was also active in Q1, with 33 announced transactions, marking a 50% increase over the prior quarter. Acquisitions were primarily driven by regional health systems looking to expand market share through strategic acquisitions.

During the quarter, Ankura’s Transaction Advisory practice provided guidance on a diverse range of deals across the sector, including transactions in acute care hospitals, dentistry, behavioral health, physician practices, and long-term care services.

Future Outlook

Looking ahead in 2026, healthcare investors will continue to monitor the cost of capital, broader economic conditions, the regulatory landscape, and the impact of Trump administration policy decisions. The Federal Reserve paused rate cuts in January 2026, and rates are expected to remain relatively steady in the near term, while inflation has moderated from prior peaks but remains above target.

At the federal level, investors should continue to expect meaningful scrutiny of healthcare transactions, particularly those involving consolidation, serial acquisitions, and private equity-backed platform strategies. The FTC’s Healthcare Task Force may contribute to a more coordinated review environment and could increase focus on transactions that raise competition, pricing, or care-delivery concerns.

At the state level, expanding review frameworks are likely to remain an important consideration, especially for private equity-backed deals and transactions involving MSO structures. Investors may face greater disclosure requirements, longer notice periods, and extended timelines as more states pursue broader review authority.

Geopolitical conflict in the Middle East could continue to impact financial conditions in the quarters ahead. If higher energy prices, inflation pressure, or market volatility persist, financing costs may remain elevated and investors may become more selective. These factors could weigh on deal activity, particularly for more leveraged transactions and sectors with greater reimbursement or labor sensitivity.

Overall, we expect transaction activity to continue building as momentum improves, although investors are likely to remain mindful of heightened regulatory scrutiny and the potential for tighter financial conditions driven by inflation and geopolitical uncertainty.

About Ankura Healthcare Transaction Advisory Services

Healthcare transactions are inherently complex. With deep industry experience, Ankura delivers insights to make informed investment decisions in mergers, acquisitions, and partnerships.

Ankura’s Healthcare Transaction Advisory team is deeply rooted in the healthcare sector, leveraging extensive industry knowledge and expertise to anticipate critical financial accounting aspects of transactions while also understanding the operational drivers. This enables us to proactively address critical financial accounting aspects and operational drivers of transactions.

What sets us apart is the collaboration between our financial accounting due diligence experts and Ankura’s specialized teams in healthcare valuation, healthcare operations, tax, information technology, commercial strategies, and human capital. This collaboration ensures a seamless, integrated reporting process to you, combining diverse expertise to provide a holistic view of every transaction. Our approach guarantees that you receive nuanced, actionable insights in a unified and strategic manner.

With senior deal professionals engaged in every transaction phase, we provide immediate updates on significant deal factors and a dedicated analysis of any critical issues, ensuring a thorough understanding and resolution of underlying concerns.

Connect with one of our Healthcare Transaction Advisory experts to navigate the complexities of healthcare with confidence. Meet our dedicated professionals below and reach out to us for more information.

Sources

[1] Scope Research Healthcare M&A Volume Database, published by Scope Research; Capital IQ

[2] The Professional Services sector includes dentistry, physical therapy, physician practices, urgent care, veterinary, and other clinics. The Outsourced Services sector includes billing, revenue cycle, management services organizations, marketing, staffing, and other services commonly outsourced by medical practices.

© Copyright 2026. The views expressed herein are those of the author(s) and not necessarily the views of Ankura Consulting Group, LLC, its management, its subsidiaries, its affiliates, or its other professionals. Ankura is not a law firm and cannot provide legal advice.