Download the Ankura U.S. Bank M&A Tracker dataset.

Key Highlights

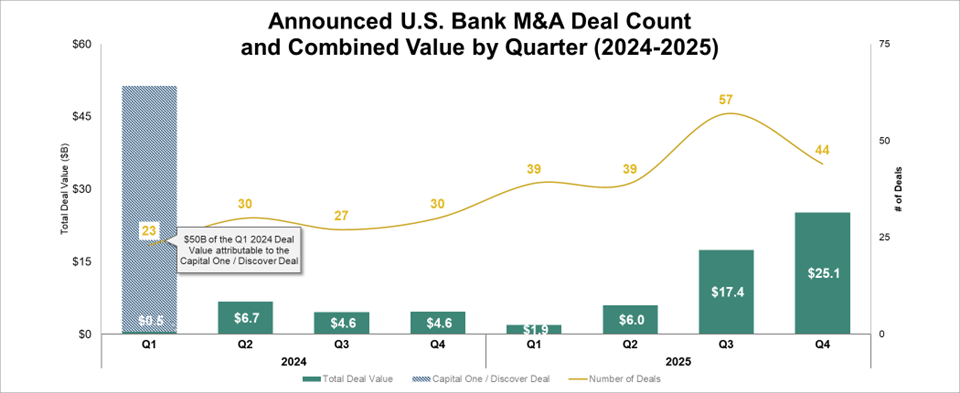

Hot Q4: The U.S. bank acquisition market finished an already strong year with 44 transactions announced in Q4 totaling $25.1 billion in total deal value.

Market Influences: Federal Reserve rate cuts throughout 2025 and more potentially on the horizon next year are projected to lower financing costs and narrow the bid-ask spread on valuations. This ease in credit conditions may serve as a catalyst to further increase deal volume across the banking sector.

Positive Outlook: The sustained flow of banking deals in 2025 signals a healthy appetite for consolidation in the banking industry with positive momentum for another active year in 2026.

Notable Q4 Transactions

Q4 2025 has seen some significant transactions announced, including:

| Deal Overview |

| Fifth Third Bancorp Acquiring Comerica: Announced in October 2025, this $10.9 billion all-stock deal is designed to create the ninth largest bank in the U.S. and accelerate Fifth Third’s expansion into high-growth markets like Texas, California, and the Southeast. The merger combines Fifth Third’s digital and retail strength with Comerica’s premier middle-market commercial franchise, while aiming to scale high-return fee businesses in payments and wealth management. |

| Huntington National Bank Acquiring Cadence Bank: Huntington Bancshares entered into a $7.6 billion all-stock agreement in late 2025 to acquire Cadence Bank, establishing a strategic presence across the South with immediate scale in Texas and Mississippi. This partnership allows Huntington to deploy its “people-first” banking playbook into high-growth metropolitan statistical areas like Houston, Dallas, and Atlanta, while leveraging Cadence’s strong local commercial relationships. |

| Nicolet Bankshares, Inc. Acquiring MidWestOne Financial Group, Inc.: This transformational $866 million merger creates one of the largest community banks in the Upper Midwest with over $15 billion in assets. The deal connects Nicolet’s Wisconsin-based footprint with MidWestOne’s presence in Iowa and Minnesota, aiming to drive peer-leading profitability through significant economies of scale and an expanded wealth management platform. |

| CVB Financial Corp. Acquiring Heritage Commerce Corp: CVB Financial Corp. is acquiring Heritage Commerce Corp for approximately $811 million to execute its long-standing strategic objective of expanding into the San Francisco Bay Area. This transformational merger creates one of California’s top 10 largest bank holding companies with approximately $22 billion in total assets, providing comprehensive geographic coverage across the state’s major business banking markets and leveraging significant operational synergies. |

| FirstSun Capital Bancorp Acquiring First Foundation Inc.: FirstSun agreed to acquire First Foundation in an all-stock deal valued at approximately $747 million in October 2025 to materially accelerate its expansion strategy in the vibrant Southern California market. The merger is designed as a “balance sheet re-positioning” that unlocks First Foundation’s core franchise while leveraging FirstSun’s commercial and industrial-focused growth strategy and specialty business capabilities. |

| Associated Bank Acquiring American National Bank: Associated Bank’s $604 million acquisition of American National Corporation aims to deepen its presence in the Twin Cities and establish a top-tier market share in Omaha. This partnership accelerates Associated’s Midwest growth strategy by adding a high-quality commercial lender and broadening its reach into the faster-growing Nebraska and Iowa markets. |

Key Themes

Large Players Enter the Market

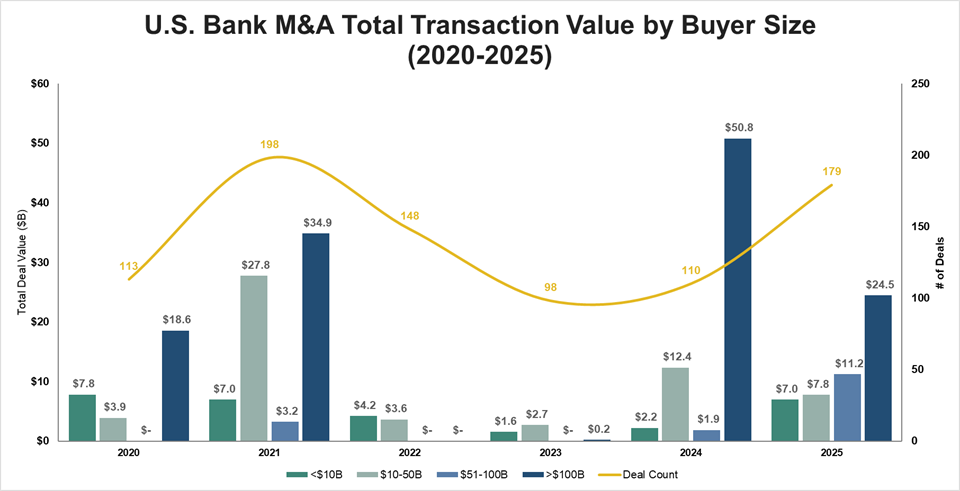

After a period of relative dormancy in 2022 and 2023, where transaction value for buyers with over $100 billion in assets was negligible, 2025 marks a pivotal return to large-scale consolidation. While 2024 headlines were dominated by a single mega-deal (Capital One/Discover), the data for 2025 reveals a broader, more structural recovery in the market. Total deal count has climbed to 179, the highest level since the 2021 peak, underpinned by a significant $24.5 billion in transaction value driven specifically by buyers in the over $100 billion asset class. This signals that large financial institutions have moved past the wait-and-see approach regarding regulatory climate and economic uncertainty and are now aggressively pursuing scale to defend margins and market share.

This trend was cemented in Q4 2025 by two marquee transactions that redefine the upper-middle market: Huntington Bank’s acquisition of Cadence Bank and Fifth Third Bancorp’s acquisition of Comerica. Unlike the opportunistic or distressed mergers and acquisitions (M&A) activity seen in previous cycles, these deals represent strategic mergers of conviction. By targeting assets in the $50-$100 billion range, buyers like Huntington and Fifth Third are effectively creating a new tier of competitors capable of rivaling the global systemically important banks in technology spend and deposit management, while maintaining the agility of regional operators.

Looking forward, this uptick in activity indicates that achieving scale is once again a primary strategic priority. The $24.5 billion deployed by large buyers this year indicates that the industry is entering a new phase of consolidation. As rates continue to come down and margins get compressed, we anticipate that super-regionals will continue to utilize M&A as their primary lever for growth, targeting complementary franchises that offer immediate balance sheet optimization and operational synergies.

The Lone Star State Shines Brightest

Texas has decoupled from the broader national banking trend, operating less as a state market and more as a standalone growth engine. With 21 transactions announced in 2025, the state has become the primary battleground for U.S. banking consolidation. The macro drivers are undeniable: Texas boasts a gross domestic product (GDP) growth rate consistently outpacing the national average, fueled by a structural migration of financial services and corporate headquarters to the Dallas-Fort Worth and Austin corridors. For acquirers, Texas offers a unique form of demographic arbitrage: By swapping capital from lower-growth Midwest or coastal markets into the high-velocity Texas ecosystem, banks can instantly re-rate their organic growth prospects. It is no longer just about gaining a footprint; it is about acquiring exposure to one of the country’s most resilient commercial lending environments.

The resurgence of the larger buyer class discussed previously has a clear geographic thesis. Historically, Texas M&A was dominated by in-market consolidation (Texas banks buying Texas banks), but the deals led by Huntington and Fifth Third represent a decisive Midwest-to-South capital flight. Their specific targets (Dallas-based Comerica and Houston-focused Cadence) reveal a deeper strategy: Midwestern powerhouses are willing to pay scarcity premiums to buy growth that does not exist in their legacy footprints. The signal is clear: The window for organic entry is shrinking, and to win in Texas today requires immediate scale, forcing outsiders to purchase established commercial networks rather than build them brick-by-brick.

This influx of external capital is likely to accelerate the scarcity value of the remaining independent Texas franchises. As these new super-regional entrants integrate their acquisitions, they will bring large scale technology and treasury capabilities to the Texas market, putting immense pressure on smaller incumbents to either scale up rapidly or seek their own exit partners. We view the Texas market not as overheated, but as undergoing a permanent structural repricing where access to the Texas commercial client base is now considered a critical asset for any bank aspiring to national relevance.

Deal Reaction as a Test of Confidence

Buyer Market Stock Price Reaction Analysis: Initial Drop vs. Recovery Time

The market’s reaction to bank M&A has shifted, moving beyond just the initial price drop to a broader test of the deal’s value. While the median day one decline in an acquirer’s stock price has improved slightly to -2.46% in this higher interest rate environment, this number hides a growing skepticism: Over 63% of transactions now trigger an immediate sell-off, an increase from previous years. The driver in today’s environment is that investors are no longer giving acquirers the benefit of the doubt. Instead of seeing large-scale integration as an immediate opportunity, many investors view it as a risk that needs to be proven before they buy back in.

The underlying data reveals a decisive shift in investor psychology that extends well beyond the initial print. Historically, post-announcement dips were a liquidity event; today, they represent a fundamental repricing of integration risk. The median max drawdown — the deepest point the stock falls post announcement — has widened to nearly 9%, signaling that the market demands a higher return for the uncertainty of the combined entity. This trend exposes a new reality for buyers: The rising tide of the zero-rate era is gone. Maintaining value today requires more than just good math on paper; it demands immediate, tangible proof that the integration is working.

This dynamic is likely to remain a core part of the consolidation landscape. With the median time to recover extending to 20 trading days, a 33% increase from the prior cycle, management teams must realize that the window for error and leniency has closed. The market is effectively signaling that a well-executed integration is no longer just an operational detail, rather the primary lever for stock price recovery. As this trend takes shape, it places significant pressure on bank leadership not just to validate the strategy, but to demonstrate flawless execution from day one. We view this extended recovery period not as a temporary blip, but as a shift where the stock price is directly tethered to the speed and success of the integration itself.

Dip in Credit Union-Bank Tie Ups

While the overall U.S. banking M&A environment is experiencing a boom, one area where it contracted is around credit union-bank acquisitions. Following a record-high of 22 such deals announced in 2024, the number of these transactions announced in 2025 has dropped over 20% with only 16 such deals announced in 2025. The emergence of these deals in recent years has been met with resistance by banking trade groups who argue that the tax-exempt status of credit unions gives them an unfair advantage and that these deals erode the tax base. One of the most vocal critics of the practice is the Independent Community Bankers of America with their proposal that the government impose an “exit fee” on credit unions acquiring banks based on a percentage of the target banks assets to recoup lost tax revenue. Some regulators are responding to the criticism. Mississippi enacted a law in 2022 requiring state-chartered banks be sold to buyers insured by the Federal Deposit Insurance Corporation (FDIC), effectively banning credit unions from these deals as they are not FDIC-insured. West Virginia passed a similar bill earlier this year that requires the survivor of a bank merger to be FDIC-insured. While the FDIC themselves rescinded a 2024 statement of policy earlier this year that explicitly included language around additional scrutiny on mergers where a credit union acquires a bank, the agency is actively conducting a reevaluation of its review process, and an updated proposal could be released in the coming months. What remains to be seen is if the specter of increased regulatory oversight will continue to have a chilling effect on credit unions seeking inorganic growth.

The Fiduciary Squeeze: Activism as a Catalyst for Consolidation

With 13 campaigns launched against banks this year, the surge in banking activism in 2025 is signaling a shift in how the market forces consolidation. We are moving past the era of demands for share buybacks and operational tweaks. Instead, a specialized class of sector-focused investors, including HoldCo Asset Management and Stilwell Value LLC, deploying a sophisticated arbitrage strategy targeting the gap between standalone value and deal potential in this view, activism has become a double-edged sword for the M&A market. On one hand, these funds function as unsolicited deal originators, spotting institutions where the highest and best use of shareholder capital is a sale to a larger peer. On the other, they are increasingly acting as governance gatekeepers for larger banks, pressuring potential acquirers to abandon this strategy in favor of share buybacks.

While the headline strategy remains forcing underperforming boards to sell, a growing subset of campaigns is targeting buyers to enforce strict pricing discipline. This tactic creates a fiduciary squeeze on directors across the industry where sellers are forced to empirically prove that independence outperforms a sell premium, while buyers are pressured to prove that M&A generates more value than returning cash to shareholders. By turning board elections into referendums on capital deployment, activists are stripping management teams of their ability to trust the process, presenting them with a binary ultimatum: Deliver superior returns through immediate action, whether via a sale or a buybacks, or hand the keys to a board that will.

Completed Deals

34 deals closed in Q4. A detailed list of these deals, along with primary and secondary reasons, is provided below:

| Ann. Date | Comp. Date | Buyer Name | Target Name | Primary Reason | Secondary Reason |

| 9/23/2025 | 12/6/2025 | Fidelity Investments | Rake Bancorporation | Geographic Expansion and Market Share Increase | |

| 9/23/2025 | 12/5/2025 | Fidelity Investments | Frost State Bank | Geographic Expansion and Market Share Increase | |

| 9/6/2025 | 11/8/2025 | Town & Country Bancorp, Inc. | Great River Bancshares, Inc. | Geographic Expansion and Market Share Increase | |

| 8/12/2025 | 11/7/2025 | American Bancorp, Inc. | New Republic Partners, Inc. | Strategic Positioning/Diversification | Scale and Efficiency |

| 8/1/2025 | 11/4/2025 | Texas National Bank | Citizens State Bank | Geographic Expansion and Market Share Increase | |

| 7/29/2025 | 12/16/2025 | Cornerstone Bank | Athol Savings Bank | Geographic Expansion and Market Share Increase | |

| 7/28/2025 | 12/6/2025 | Park State Bank | First National Bank | Geographic Expansion and Market Share Increase | |

| 7/23/2025 | 12/1/2025 | Colony Bankcorp, Inc. | TC Bancshares, Inc. | Geographic Expansion and Market Share Increase | Scale and Efficiency |

| 7/23/2025 | 11/11/2025 | Campbell County Bank | Farmers State Bank | Geographic Expansion and Market Share Increase | Enhanced Product/Service Offerings and Capabilities |

| 7/22/2025 | 12/31/2025 | Mercantile Bank Corporation | Eastern Michigan Financial Corporation | Geographic Expansion and Market Share Increase | |

| 7/18/2025 | 10/1/2025 | BankSouth | State Bank of Cochran | Geographic Expansion and Market Share Increase | Strategic Positioning/Diversification |

| 7/14/2025 | 10/20/2025 | Huntington Bancshares | Veritex Holdings, Inc. | Geographic Expansion and Market Share Increase | Strategic Positioning/Diversification |

| 7/10/2025 | 11/6/2025 | Civista Bank | Farmers Savings Bank | Geographic Expansion and Market Share Increase | |

| 7/3/2025 | 11/8/2025 | Regional Missouri Bank | Bank of New Cambria | Geographic Expansion and Market Share Increase | |

| 6/24/2025 | 10/1/2025 | Glacier Bancorp, Inc. | Guaranty Bancshares, Inc. | Geographic Expansion and Market Share Increase | |

| 6/23/2025 | 10/11/2025 | Peoples Savings Bank of Rhineland | Farmbank | Geographic Expansion and Market Share Increase | |

| 6/23/2025 | 11/1/2025 | First Financial Bancorp. | Westfield Bancorp | Geographic Expansion and Market Share Increase | |

| 6/12/2025 | 10/4/2025 | Bendena State Bank | Bank of Denton | Geographic Expansion and Market Share Increase | |

| 6/10/2025 | 10/1/2025 | Millennium Bancshares, Inc. | North Georgia Community Financial Partners, Inc. | Geographic Expansion and Market Share Increase | |

| 6/5/2025 | 11/14/2025 | NB Bancorp, Inc. | Provident Bancorp, Inc. | Scale and Efficiency | |

| 5/29/2025 | 10/1/2025 | Seacoast Banking Corporation of Florida | Villages Bancorporation, Inc. | Geographic Expansion and Market Share Increase | Strategic Positioning/Diversification |

| 5/21/2025 | 11/17/2025 | BancFirst Corporation | American Bank of Oklahoma | Geographic Expansion and Market Share Increase | Scale and Efficiency |

| 5/20/2025 | 11/1/2025 | Hometown Financial Group, Inc | CFSB Bancorp, Inc. | Geographic Expansion and Market Share Increase | |

| 5/1/2025 | 10/6/2025 | Bank of Commerce | Holmes County Bank | Geographic Expansion and Market Share Increase | Enhanced Product/ Service Offerings and Capabilities |

| 5/1/2025 | 10/1/2025 | First National Bank of Omaha | CCB Financial Corporation | Geographic Expansion and Market Share Increase | |

| 4/25/2025 | 10/31/2025 | Regent Capital Corporation | DLP Bancshares, Inc. | Scale and Efficiency | Geographic Expansion and Market Share Increase |

| 4/24/2025 | 10/1/2025 | Miners and Merchants Bancorp, Inc. | First Community Corporation | Geographic Expansion & Market Share Increase | |

| 4/24/2025 | 10/28/2025 | Eastern Bankshares, Inc. | HarborOne Bancorp, Inc. | Geographic Expansion and Market Share Increase | Scale and Efficiency |

| 4/23/2025 | 10/1/2025 | Citizens & Northern Corporation | Susquehanna Community Financial, Inc. | Geographic Expansion and Market Share Increase | Scale and Efficiency |

| 3/18/2025 | 10/1/2025 | Legacy Community Federal Credit Union | First Community Bank of Cullman | Strategic Positioning/Diversification | Geographic Expansion and Market Share Increase |

| 3/17/2025 | 12/1/2025 | MetroCity Bankshares, Inc. | First IC Corporation | Geographic Expansion and Market Share Increase | Scale and Efficiency |

| 3/4/2025 | 10/10/2025 | Battle Financial, Inc. | Stearns Bank of Upsala, National Association | Strategic Positioning/Diversification | Geographic Expansion and Market Share Increase |

| 11/8/2024 | 11/3/2025 | DFCU Financial | Winter Park National Bank | Strategic PositioningDiversification | Geographic Expansion and Market Share Increase |

| 4/22/2024 | 10/4/2025 | Freedom Bancshares, Inc. | Appalachian Financial Corporation | Scale and Efficiency | Geographic Expansion and Market Share Increase |

Looking Ahead

The positive momentum observed in the U.S. banking M&A market has continued its upward trajectory into the latter half of the year, suggesting renewed confidence that a period of robust and healthy consolidation lies ahead. The core strategic drivers pushing institutions toward mergers remain compelling: the urgent need to achieve critical scale to spread escalating technology costs, the imperative to capture operational efficiencies, and the desire to expand into new and high-growth markets. Although the persistent challenge of elevated interest rates continues to exert pressure on deal valuations, the recent reduction in rates and shifting regulatory attitude towards mergers are reducing uncertainty and bolstering confidence among buyers and sellers. This confluence of strategic growth needs and improved regulatory visibility points toward a continued favorable climate for bank M&A throughout 2026. Strategic combinations will remain the primary mechanism for institutions seeking to adapt, grow, and secure their position in an evolving financial landscape.

How Ankura Can Help

Ankura plays a crucial role in this process by providing expert guidance and tailored solutions throughout the M&A lifecycle. With deep industry knowledge and experience, our experts assist banks in identifying strategic opportunities, conducting thorough due diligence, and managing post-merger integrations. Our comprehensive approach ensures that banks can maximize synergies, mitigate risks, and achieve desired outcomes, ultimately driving successful M&A transactions that align with their long-term strategic objectives.

Related Insights

Banking Industry Outlook: U.S. Banking M&A Surge Arrives in Q3

Banking Industry Outlook: U.S. Banking M&A Activity Mid-Year Review

Banking Industry Outlook: Potential Surge in Banking Mergers and Acquisitions

Methodology/Data Sources

The M&A transaction data presented in this report is compiled through extensive research of publicly available information. Our dataset includes transactions where either: 1) Banks are acquiring other banks; or 2) Banks are being acquired by non-bank financial institutions.

Our primary data sources for identifying and verifying these transactions include:

- Public Announcements and Press Releases: We monitor news wires and company-specific press releases for official announcements of M&A agreements.

- Regulatory Filings: Key regulatory bodies provide valuable public information. This includes, but is not limited to, filings with the Securities and Exchange Commission for public companies. For financial institutions, we also consult filings with the FDIC, the Federal Reserve, and other relevant state and federal banking regulators.

- Financial News Outlets and Industry Publications: Reputable financial news services and banking industry-specific publications are monitored for reported transactions and market intelligence, which are then cross-referenced with official sources.

- Proprietary Databases and Aggregators: While the core data is derived from public sources, we also leverage and cross-reference information from commercial M&A databases and data aggregators that synthesize publicly available financial and transaction data to ensure comprehensive coverage and accuracy.

Each identified transaction is carefully reviewed to confirm its nature, deal value, participants, and announcement/completion dates, ensuring the integrity of our M&A transaction dataset.

© Copyright 2026. The views expressed herein are those of the author(s) and not necessarily the views of Ankura Consulting Group, LLC, its management, its subsidiaries, its affiliates, or its other professionals. Ankura is not a law firm and cannot provide legal advice.